Blog & News

SHADAC in AJPH: Insurance-Based Discrimination Reports and Access to Care Among Non-Elderly U.S. Adults, 2011-2019

December 8, 2022:This journal article was originally published in the American Journal of Public Health (AJPH).

Authors: Kathleen Thiede Call, PhD, Giovann Alarcon-Espinoza, PhD, MPP, Natalie Schwer Mac Arthur, PhD, MAc, and Rhonda Jones-Webb, DrPH

SHADAC researchers and external co-authors recently published an article in the American Journal of Public Health (AJPH) that examines rates of insurance-based discrimination for nonelderly adults with private, public, or no insurance between 2011 and 2019, a period marked by passage and implementation of the Affordable Care Act (ACA) and threats to it.

SHADAC researchers and external co-authors recently published an article in the American Journal of Public Health (AJPH) that examines rates of insurance-based discrimination for nonelderly adults with private, public, or no insurance between 2011 and 2019, a period marked by passage and implementation of the Affordable Care Act (ACA) and threats to it.

Using 2011–2019 data from the biennial Minnesota Health Access Survey, the study found that about 4,000 adults aged 18 to 64 report insurance-based discrimination experiences. Using logistic regressions, the authors examined associations between insurance-based discrimination and (1) sociodemographic factors and (2) indicators of access.

Key Findings

- On average, approximately 10% of nonelderly adults reported insurance-based discrimination, although there was a statistically significant increase from 7.7% in 2015 to 11.0% in 2017.

- Reports of insurance-based discrimination remained remarkably stable within each coverage type between 2011 and 2019:

- Uninsured adults ranged between 24.7% to 28.1%

- Adults with public coverage ranged between 18.4% to 24.0%

- Adults with private coverage ranged between 3.0% to 5.4%

- Compared with adults with private insurance (4% on average), insurance-based discrimination was 5 or 6 times higher for adults with public insurance (21% on average) and about 7 times higher for adults with no insurance (27% on average).

- There was little association between insurance-based discrimination and having a usual source of care. However, insurance-based discrimination persistently interfered with confidence in getting needed care and reports of forgone care.

These findings indicate that policy changes from 2011 to 2019 affected access to health insurance, but high rates of insurance-based discrimination among adults with public insurance or no insurance were impervious to such changes. Stable rates of insurance-based discrimination during a time of increased access to health insurance via the ACA suggest deeper structural roots of healthcare inequities.

Read the full American Journal of Public Health article to learn more about the study methods and findings. A copy of this AJPH article is also available upon request.

Blog & News

California Health Insurance Stable in 2021, but Many Will Need to Switch Coverage Once COVID-19 Pandemic Protections End (CHCF Cross Post)

November 4, 2022:The following content is cross-posted from California Health Care Foundation published on November 4, 2022.

Authors: Colin Planalp and Lacey Hartman, SHADAC

Employer-sponsored insurance declined significantly; Medi-Cal and individual market coverage held steady

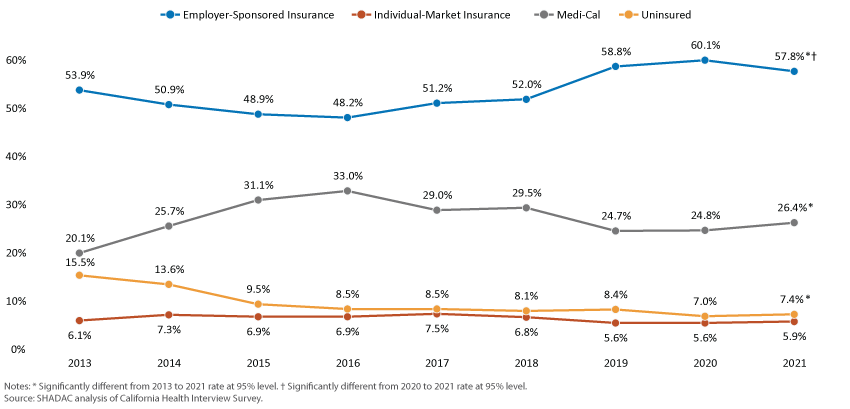

During 2021, the second calendar year of the COVID-19 pandemic, California’s health insurance landscape remained relatively stable. This article focuses exclusively on Californians under age 65, which is the threshold for age-based Medicare coverage, and the coverage rates highlighted below include children except where otherwise specified (i.e., “nonelderly adults”). Based on the 2021 California Health Interview Survey (CHIS), the percentage of Californians under age 65 without health insurance, 7.4% in 2021, was not significantly different from the prior year. There also were no statistically significant changes across demographic groups, including income, age, geography, and race and ethnicity.

Also, the rate of Californians with individual market coverage, 5.9% in 2021, was statistically unchanged from 2020. While the rate of Californians with Medi-Cal coverage (California’s Medicaid program), 26.4% in 2021, appears higher than the 24.8% of 2020, the difference is not statistically significant. That finding contrasts with records from the California Department of Health Care Services, which reported that Medi-Cal enrollment increased by 7.3% (893,552 enrollees) in 2021 for people under age 65, growing from 12,244,085 in December 2020 to 13,137,637 in December 2021.1

There are multiple potential explanations why survey data on Medi-Cal enrollment may differ from Medi-Cal’s records. Research shows that surveys tend to undercount people enrolled in state Medicaid programs, in part due to people’s confusion over program names and whether they are still enrolled in Medicaid. This second issue, of people being unaware they are still enrolled, may have been exacerbated during the pandemic. A temporary policy, termed “continuous coverage,” prevented enrollees from being disenrolled from Medicaid during the public health emergency, as health coverage has been vital to preserving access to health care. This policy may have resulted in some Californians retaining Medi-Cal coverage they assumed had expired.

Health Insurance in California by Coverage Type, 2013–21

At the same time, the rate of Californians with employer-sponsored insurance (ESI) declined significantly, from 60.1% in 2020 to 57.8% in 2021. The losses in ESI appear to have been offset by increases in Medi-Cal coverage for some key groups. For instance, while ESI rates declined significantly for nonelderly adults (age 18–64), people with moderate incomes (139%–400% of federal poverty level) and Latinx people experienced statistically significant increases in Medi-Cal coverage rates. 2

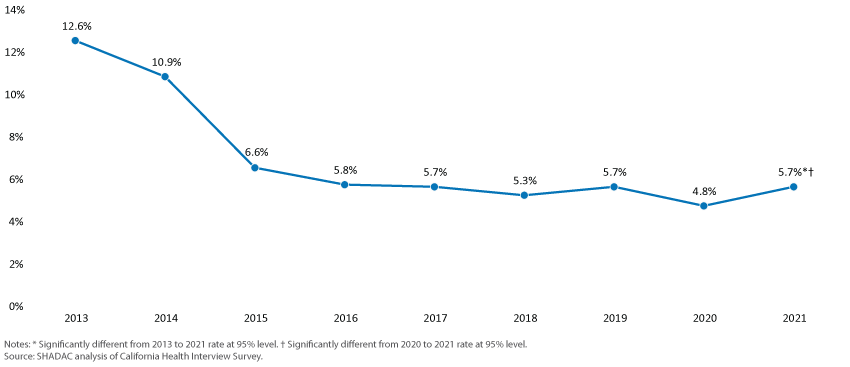

Although the percentage of Californians without health insurance at a given time was unchanged in 2021, the rate of Californians experiencing long-term uninsurance (for a year or more) rose from 4.8% in 2020 to 5.7% in 2021, a statistically significant increase.

Conclusions and Discussion

Overall, the stability of the state’s health insurance rate can be seen as positive, particularly during the upheaval of the COVID-19 pandemic. Despite massive job losses in 2020, California’s uninsurance rate declined to a historic low in the first year of the pandemic, almost certainly due to federal and state efforts to maintain or improve access to health insurance. The ability for California to hold that low rate of uninsurance into a second volatile year of the pandemic is notable.

There were other measures, however, that indicate California’s coverage landscape shifted slightly since 2020. For instance, the state’s rate of ESI coverage declined significantly in 2021, which would be concerning if it developed into a trend. However, it is important to recognize that in 2020 the portion of Californians with ESI was a high-water mark since full implementation of the Affordable Care Act in 2014, so it could be that the trend of increased ESI in recent years is only moderating.

Another potentially concerning indicator was the increase in California’s rate of long-term uninsurance from 2020 to 2021. But in this case, trend data show that the 2020 long-term uninsurance rate of 4.8% may simply have been an outlier — possibly to due to the pandemic — with the 2021 rate of 5.7% falling back in line with the narrow range of rates between 5.3% and 5.8% for other years since 2016.

Altogether, data from the 2021 CHIS illustrate a surprisingly stable landscape of health insurance coverage. The COVID-19 pandemic — which began in 2020 and continued into 2021 and beyond — had the potential to cause massive losses of health insurance coverage, primarily through declining ESI caused by sharp job losses. But uninsurance rates did not spike, and ESI coverage has not shown dramatic erosion compared to the prepandemic trend.

Even as the pandemic persisted into 2022, many of the government supports that helped people maintain coverage during the crisis have already ended or are expected to sunset soon. For example, the growth of Medi-Cal coverage for key subpopulations during the pandemic is due in large part to the continuous coverage provision associated with the public health emergency, expected to end sometime in 2023. While researchers project that most Californians losing Medi-Cal will be eligible for other types of coverage, as CHCF has written elsewhere, it will be critical to take action to keep enrolled those who continue to be eligible for Medi-Cal, and to connect those who become ineligible to alternative sources of coverage. This — as well as other challenges, such as inflation — may make holding onto California’s coverage gains difficult. To fully understand whether and what kinds of impacts the pandemic triggered in California’s health coverage landscape, it will be vital to continue monitoring data from 2022 and future years.

Notes

1 Wilson Analytics analysis of “Month of Eligibility, Race/Ethnicity, and Age group, by County, Medi-Cal Certified Eligibility” (Jan. 2010–March 2022), California Health and Human Services Open Data portal.

2 Groups typically eligible for Medi-Cal above 138% FPL include children, pregnant women, and some disabled people. However, due to the continuous coverage provision under the federal COVID-19 public health emergency, some whose incomes rose above the 138% threshold may have temporarily retained Medi-Cal coverage, even though they would have lost eligibility under normal circumstances.

Blog & News

Key Resources and 2022 Updates: SHADAC's Health Insurance Unit

October 2022:Updated April 2023

In the years following the passage of the Patient Protection and Affordable Care Act (ACA), SHADAC developed and introduced its Health Insurance Unit, or “HIU,” a tool to aid in defining family interrelationships in federal population surveys for the purpose of analyzing health insurance coverage.

Since the inception of this tool, SHADAC has regularly produced updated HIU variables, including in fall 2022 following the release of the 2021 American Community Survey (ACS) and 2022 Current Population Survey Annual Social and Economic Supplement (CPS ASEC). These variables were recently made available via IPUMS-CPS (October 19, 2022) and IPUMS-USA (March 10, 2023). These HIU variables use the updated HIU methodology introduced in 2020 and incorporate the latest years of survey data and federal poverty guidelines, as relevant.

What is the SHADAC HIU?

First released in 2012, one of the goals of the SHADAC HIU is to establish a common definition of a “family unit” to help ensure consistent and comparative research across major national surveys when analyzing health insurance coverage.

Most federal surveys define a “family” differently from the way it is defined by most private and public insurance programs. For instance, the definition of "family" or "household" in U.S. Census Bureau surveys includes all related members of a household, no matter the degree of relationship, and does not necessarily align with dependent coverage or public program eligibility.

The SHADAC HIU attempts to more closely align with a definition of family used for private and public health insurance coverage eligibility. The SHADAC HIU uses a narrower definition of family that looks at specific interrelationships between individuals within a household and excludes all non-dependent relatives (grandparents, adult siblings, aunts/uncles, etc.) who may be household members but are unlikely to be considered as part of the “family unit” as defined for the purposes of determining eligibility for health insurance.

The SHADAC HIU, then, is defined as an economic unit that consists of those members of a household who would likely be eligible as a group for family health insurance coverage, or whose resources (i.e., income) would be considered in determining eligibility for public coverage.

Related Resources

- Defining Family for Studies of Health Insurance Coverage (August 2021): A brief that outlines the impacts of using the SHADAC HIU in analysis—specifically, analysis showing how the population distribution of family income changes using three different definitions of family: all members in the same household (Census definition), the definition used by the IPUMS (described below), and the SHADAC HIU (described in detail in a companion brief). Researchers can use this brief to assess whether the SHADAC HIU is suitable for their analysis and what the potential impacts of its use might be.

- Stata Code (January 2021): Technical documentation of statistical code in STATA to help researchers to employ the SHADAC HIU in their own analysis using ACS microdata downloaded from IPUMS USA.

Publication

Comparing Federal Government Surveys That Count the Uninsured: 2022

With the release of new insurance coverage estimates from surveys conducted by the U.S. Census Bureau, the Agency for Healthcare Research and Quality (AHRQ), and the Centers for Disease Control and Prevention (CDC), SHADAC has updated our annual “Comparing Federal Government Surveys that Count the Uninsured” brief.

The brief provides an annual update to comparisons of uninsurance estimates from four federal surveys:

- The American Community Survey (ACS)

- The Current Population Survey (CPS)

- The Medical Expenditure Panel Survey - Household Component (MEPS-HC)

- The National Health Interview Survey (NHIS)

In this brief, SHADAC presents current and historical national estimates of uninsurance along with the most recent available state-level estimates from these surveys (where possible). We also discuss the main reasons for variation in the estimates across the different surveys as well as possible reasons for incomparability of estimates across and within the surveys.

Download a PDF of the Comparing Federal Government Surveys Brief.

Last year’s brief with data from the 2020 collection year, and certain 2019 collection-year data, can be accessed here.

Publication

An Annual Conversation with the U.S. Census Bureau: Health Insurance Coverage Estimates from the 2021 ACS and CPS (Webinar)

SHADAC hosted a webinar on Thursday, September 29, 2022 that provided an overview of 2011 health insurance coverage estimates from two key, large-scale federal data sources: The American Community Survey (ACS) and the Current Population Survey (CPS).

This webinar examined the new estimates at both the national and state levels, as well as by coverage type, with technical insight from experts at the U.S. Census Bureau, which administers both the ACS and CPS, and from SHADAC researchers.

Attendees learned about:

- The new 2021 national and state coverage estimates

- When to use which estimates from which survey

- How to access the estimates via Census reports and the data.census.gov website

- How to access state-level estimates from the ACS using SHADAC tables

SHADAC researchers and Census experts also answered questions from attendees after the presentation.

Download the slide deck from this webinar here.

Speakers

Kathleen T. Call, Moderator

Investigator

SHADAC Dr. Call has been an Investigator with SHADAC since its launch in 2001. She is also a Professor in the Division of Health Policy and Management at the University of Minnesota (UMN), School of Public Health (SPH). She demonstrates her commitment to community-engaged scholarship through her leadership in the Clinical and Translational Science Institute, and the Interdisciplinary Research Leaders (IRL) program, and by co-chairing the UMN, SPH Health Equity Work Group.

|

Sharon Stern, Speaker

Assistant Division Chief

United States Census Bureau Sharon Stern is assistant division chief for employment characteristics in the U.S. Census Bureau’s Social, Economic and Housing Statistics Division. In her position, Stern oversees statistics on the labor force, health insurance and disability from several Census Bureau surveys. She has authored Census Bureau reports and papers on topics related to poverty, disability and health insurance.

|

Robert Hest, Speaker

Research Fellow

SHADAC Robert Hest joined SHADAC in 2017 as a Research Fellow. Mr. Hest provides expertise in survey data, data analysis and processing, and project management and tracking. Mr. Hest manages SHADAC’s State Health Compare website, coordinating data processing, quality assurance, dissemination, and documentation of data.

|

Laryssa Mykyta, Speaker

Chief of Health and Disability Statistics Branch

United States Census Bureau Laryssa Mykyta is chief of the Health and Disability Statistics Branch in the Social, Economic, and Housing Statistics Division at the U.S. Census Bureau. The Health and Disability Statistics Branch is responsible for analyzing and publishing data collected on health insurance coverage, health status and health care utilization, and disability.

|

Katherine Keisler-Starkey, Speaker Katherine Keisler-Starkey, SpeakerEconomist in Health and Disability Statistics Branch United States Census Bureau Katherine Keisler-Starkey is an economist in Health and Disability Statistics Branch in the U.S. Census Bureau’s Social, Economic and Housing Statistics Division. In her position, Starkey performs research and works as a subject matter expert on health topics for the Current Population Survey Annual Social and Economic Supplement. She has authored the Census Bureau’s Health Insurance Coverage in the United States report for the last three years. |