Basics Blog

SHADAC has created a series of “Basics Blogs” to familiarize readers with common terms, concepts, and topics that are frequently covered. See all Basics Blogs here.

Health care costs have been rising at an alarming rate in the U.S., and patients and households are increasingly expected to bear the burden. National health expenditures grew 7.5% in 2023 alone, reaching $4.9 trillion, or $14,570 per person.1

A recent Gallup study found that a record number of Americans struggle to afford quality medical care, with nearly 29 million people considered “Cost Desperate,” meaning they lack access to quality, affordable care and have recently been unable to pay for needed care and medicine.

Along with research studies such as these, health surveys are one way to monitor trends in cost and affordability, and they have become more detailed over time. Surveys often include questions about health insurance costs (e.g., premiums and deductibles) and affordability questions that touch on consumers' increased share of financial burden, forgone care, changes to prescriptions, and medical debt. These questions offer unique insight into how the rising financial burden of health care costs impacts people's decisions and access to care.

At the federal level, the American Community Survey (ACS) and the Current Population Survey (CPS), both fielded by the U.S. Census Bureau, have long been go-to resources for analyzing these topics by asking participants about health insurance costs – primarily focusing on insurance premiums, subsidies, and employer contributions. CPS also asks detailed questions about total out-of-pocket medical spending and non-prescription health care spending over the course of a year.

Many states also conduct their own surveys asking individuals about their experience paying for and affording health care. Many states go beyond premiums and deductibles and ask about delayed care, skipped prescriptions, unpaid bills, and medical debt, offering greater context about how financial strain affects individuals’ health care use and well-being. Such context gives states greater flexibility to explore population-specific (and state-specific) concerns that can help inform policy decisions at the state level.

As part of its core activities, SHADAC regularly tracks statewide household (and employer) surveys about health coverage and access. In conjunction with the latest state-level data collection update for 2023 and 2024, this Basics Blog will explore the concepts of cost and affordability by defining key terms and summarizing how these most recent household surveys are asking health care consumers about these topics.

How Do We Define Health Insurance Costs and Affordability?

Spending on health care is a topic that is often talked about, but what does it mean, exactly? While the terms ‘health care costs’ and ‘health care affordability’ are often used interchangeably, they have some key distinctions that are important to note.

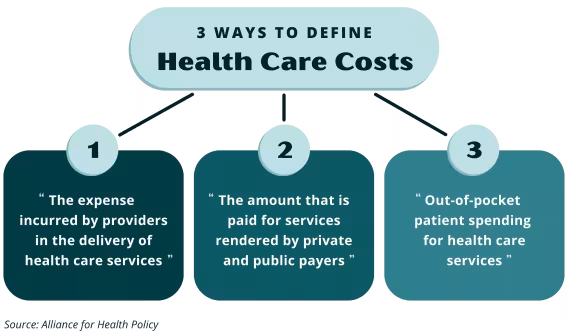

The Alliance for Health Policy, a nonpartisan health policy organization, defines health care costs as:

"Health care costs can be defined in three ways: 1) the expense incurred by providers in the delivery of health care services, 2) the amount that is paid for services rendered by private and public payers, and 3) out-of-pocket patient spending for health care services."

Health care affordability, however, emphasizes the burden placed on consumers over specific expenses. The University of Pennsylvania Leonard Davis Institute of Health Economics defines affordability as "a qualitative ability and willingness to pay – a function of income, spending, and judgments about the value of goods and services for their price."

It is important to note that these two terms can have different meanings depending on who is asked, as providers, insurers, and patients may all have distinct perspectives about costs and affordability, so these two definitions are not all-encompassing.

Health Care Costs & Medical Debt

Medical debt is another essential topic that is a part of the discussion on health care costs and affordability. The National Consumer Law Center defines medical debt as "a debt arising from the receipt of health services," with such debt being incurred because of medical costs that a person or family cannot pay during or after care.

A Peterson-KFF Health System Tracker analysis found that nearly 20 million U.S. adults have medical debt, with about 14 million people owing more than $1,000. Furthermore, the analysis found that about 3 million U.S. adults owe more than $10,000 in medical debt.

Many households who face such circumstances may resort to using credit cards, taking out loans, depleting their savings, or cutting back on necessities such as food. In severe cases, medical debt can lead to bankruptcy and long-term financial instability in households.

Collecting Data on Out-of-Pocket Spending in State-Level Household Health Surveys

While there are clearly many ways to address health care spending and financially related issues, this blog primarily focuses on cost, more specifically on the third category of the definition we reviewed earlier: out-of-pocket spending.

In this section, we examine specific aspects of how individuals and families experience financial strain related to health care and insurance costs, such as premiums, deductibles, cost-sharing responsibilities, and medical debt.

To analyze how states capture these financial concerns and topics in their surveys, we first outline our approach to identifying and categorizing relevant questions in the ‘Methods’ section. Then, in the ‘Findings’ section, we will review the questions we identified as pertaining to collecting respondents’ data on health care costs (specifically out-of-pocket spending), and look at how methods & questions differ between different states’ surveys.

While the specific questions can (and do) differ between states and surveys, we plan to walk through various examples of how states work to understand how similar concerns about finances and health affect their populations.

Methods

SHADAC recently refreshed its annual scan of all U.S. states and territories household and employer surveys about health insurance coverage, access, and costs (visit the State Survey Research Activities webpage to access this helpful resource). In this most recent update, SHADAC identified 30 states that fielded household surveys and 17 states that fielded employer surveys in the past two years (2023-2024).

For this blog, we conducted a deep dive into household surveys that assessed the following key cost and affordability domains:

- Health Care & Insurance Costs (e.g., premiums, deductibles, and employer contributions)

- Effects on Consumer Behaviors (e.g., delaying or forgoing medical, dental, or mental health care)

- Direct Financial Impact of Medical Care (e.g., out-of-pocket spending, medical debt, unpaid bills)

Note: While this blog focuses only on household surveys, employer surveys can also offer critical insight into access and coverage through job-based health insurance, a key component of affordability for many. Learn more about employer-sponsored insurance coverage in this SHADAC brief.

*Hover over a state and click the “Instrument” link to access that state’s survey instrument

**Figure 1 Note: California and Ohio have multiple instruments for the same survey used for different survey methods (i.e., telephone, online, paper).

Of the 30 states in the survey scan, eight (8) states made their survey questionnaires publicly available and were analyzed for inclusion of questions related to the outlined cost and affordability topics. The eight states’ questionnaires analyzed were from California, Colorado, Louisiana, Massachusetts, Ohio, Oregon, Rhode Island, and Wisconsin.2

Findings

The following are our findings from this survey analysis of eight (8) state health surveys:

1. Health Care & Insurance Costs

We found that nearly all the surveys across the eight-state sample go beyond asking about coverage rates and explore the overall cost burden of maintaining insurance.

Premiums were discussed in four of the eight states, where survey questions asked respondents how much they pay in premiums and whether they presented a financial burden.

Questions pertaining to deductibles were asked by six states, often including questions to help respondents understand the concepts before asking about their impact.

California was the only state to include questions about employer contributions to consumers’ or their households' health plans. California’s survey was also unique in asking questions about exploring the difficulties of finding or maintaining affordable coverage.

2. Effects on Consumer Behaviors

Delaying or Forgoing Care. Seven of eight states included questions about whether people delayed or skipped care due to cost, highlighting many states' efforts to capture behaviors linked to affordability. Specifically, respondents were asked whether they skipped or delayed general medical care in five of eight states, and the same number of states asked respondents whether they had skipped or delayed accessing prescription medications.

To gain a better understanding of how cost and affordability impacts the overall experience of consumers' health care journey, many states take a broader recognition of whole-person health by asking questions about a range of services that may have been delayed or skipped outright. Four of eight surveys asked about mental health and six asked about dental services gaps. Five states’ surveys included or prompted respondents to indicate if they had missed out on any specialty care, such as vision services or treatment for underlying conditions, highlighting potential efforts to understand issues with chronic or advanced care needs.

Forgoing or Losing Health Insurance Coverage. Seven of the eight questionnaires inquired about why individuals lost or remained without health insurance coverage, typically through multiple-choice formats that list “cost or affordability” as an answer choice. This allows states to quantify the number of respondents who cite financial problems as a barrier to maintaining coverage.

3. Direct Financial Impact of Medical Care

Medical Bills, Out-of-Pocket Spending, and Expenses. Half of the eight state surveys explicitly asked about specific out-of-pocket dollar amounts paid by consumers for health care, medical bills, etc. Some states went even further to explore the "felt experience" of medical expenses, with five states asking respondents how affordability affected them after receiving services.

These questions focus on individual or household perceptions, offering a different perspective on how cost shapes access and behavior both before and after services or care.

Medical Debt. Six states asked respondents if they had incurred medical debt, which all surveys generally defined as outstanding medical bills that could not be paid off or were being paid off over time. Only two states requested an estimate of the amount of debt, providing response options that ranged from less than $1,000 to $10,000 or more.

Just three states asked respondents follow-up questions about the effects of having medical debt, such as needing to use up savings, taking out loans, relying on credit cards, cutting back on necessities such as food or housing, or even filing for bankruptcy.

Key Takeaways of Survey Questions & Future Considerations

While the eight state health surveys that SHADAC analyzed vary in format and scope, several common threads emerged in how they approach the topics of cost and affordability.

Broad Recognition of Cost-Related Barriers

Most states included questions about financial challenges that affected access to care, particularly around skipped or delayed care due to cost. However, the depth and specificity of these questions varied, as some states focused on specific dollar amounts, while others emphasized more general perceptions of cost burden.

Despite these differences, the broad scope of questions suggests that there may be a growing consensus that cost and affordability concerns may be critical to understanding health care access and utilization – not just coverage.

A Broader View of Health Care

Some states appear to be moving beyond general questions about medical care access to better understand how cost and affordability affect different dimensions of care, including mental health, dental services, specialty care, and other areas.

Medical Debt Is Common – But Often Underexplored

Although a clear majority of states in this analysis (six of eight) asked about medical debt, only a small subset asked participants to quantify the amount or describe its impact. Questions that prompted participants to explain how debt affected their day-to-day finances, such as needing to cut back on necessities or file for bankruptcy, were rare, pointing to a potential gap in understanding health-related debt across states.

Overall, these survey insights show shared priorities and opportunities for deeper exploration across states. It is our hope that this blog post highlights the work being done at the state level to further understand the cost and affordability challenges consumers face.

Future work can build upon these insights to further strengthen the quality of data collection efforts and leverage this work to encourage even more states to conduct statewide health surveys that assess the growing needs of consumers all over the country.

To keep learning about this topic, check out our other publications that discuss using survey data to collect health information and answer public health & health policy questions.

[1] Centers for Medicare & Medicaid Services (CMS). National Health Expenditure Data: Historical. https://www.cms.gov/data-research/statistics-trends-and-reports/national-health-expenditure-data/historical