Basics Blog

SHADAC has created a series of “Basics Blogs” to familiarize readers with common terms, concepts, and topics that are frequently covered. See all Basics Blogs here.

The health care system in the U.S. can be confusing to navigate. More than half of insured adults report that they have some difficulty understanding parts of their health insurance. This can be further complicated by the many different kinds of health insurance coverage available, including:

- Employer-sponsored insurance, or “ESI”;

- Medicaid/CHIP;

- Medicare;

- Individual marketplace plans.

While distinct in their specifics, health insurers use common terminology when referring to certain parts of these plans, such as “copays,” “deductibles,” and “premiums,” among many others. But, what is a deductible? What are health insurance premiums? What is a copay, coinsurance, etc.?

This Basics Blog aims to provide high-level definitions for common health insurance terms. Beyond health insurance definitions, we also explain the context behind their use, their meaning within insurance plans, and how a better understanding of health insurance terminology can help consumers compare different types of insurance plans.

Keep reading to learn more!

What Is ESI? Employer-Sponsored Health Insurance

While we mentioned earlier that there are many types of health insurance in the U.S. (e.g., Medicaid, Medicare, Marketplace, etc.), within this blog, SHADAC will provide examples of concepts within the context of an ESI plan.

What is ESI? ESI is employer-sponsored health insurance, often just called “employer-sponsored insurance,” or “ESI.” This is health insurance that is provided by employers to employees, with coverage options for family or dependents often included.

ESI is the dominant form of health insurance coverage in the United States, with 54.7% of Americans, or roughly 182.3 million people, getting their insurance from an employer in 2023, or the employer of a family member (e.g., a spouse or parent).

For private-sector workers, ESI plays an even larger role—68.8% of eligible private-sector workers in the U.S., or roughly 63.7 million individuals, were enrolled in ESI in 2023.

Because the majority of Americans have ESI as their primary source of coverage, the definitions in this blog are written in the context of ESI plans. However, health insurance terminology is generally universal, meaning these definitions will help in understanding many plan and insurance types.

Before diving into how specific plans may operate, let’s first familiarize ourselves with what some of these terms mean.

Common Insurance Term Definitions

Although not exhaustive, the following list of terms are commonly used by different health plans and helpful to know when navigating which plan to choose or gaining a better understanding of your current coverage.

Premium

A health insurance premium is the amount paid monthly (or annually) to maintain health insurance coverage. In ESI, the cost of premiums is often split between employee and employers, with the latter typically paying a larger portion of the share.

The portion that employees are expected to pay is commonly known as the “employee contribution.” Explore average employee contributions by year, plan type, and more on State Health Compare.

Deductible

A health insurance deductible is the amount that individuals and/or families (depending on plan type) must pay out of pocket before their health insurance begins to cover the cost of medical expenses.

Depending on the type of plan, a deductible can be set up for a whole coverage period (one year) or be applied per service or procedure. It’s important to review your plan to know which type of deductible you may have.

Using MEPS survey data, State Health Compare lets you explore average annual ESI deductibles over time, by state, and more. For example, we can see in the interactive SHC chart below that in 2002, the average deductible for a family plan in the U.S. was less than $1,000 ($958). In 2023, the average has more than tripled to $3,733.

Chart 1. Average Annual ESI Family Plan Deductible Cost in U.S., 2002–2023

Copayment (Copay)

A copay is a fixed amount (for example, $15) paid for a covered health care service or prescription, usually paid when receiving the service or medication. For example, you might pay a copay when seeing your primary care doctor, or at the pharmacy picking up a prescription.

The amount can vary by the type of covered health care service, meaning you might pay a different amount for a scheduled visit to your primary care doctor versus a visit to a specialist. Copays can also vary by type of prescription or medication.

Coinsurance

Coinsurance is the percentage of the cost of a service owed by an individual after the deductible is met. For example, if a plan has a 20% coinsurance for a service costing $100, you would owe $20.

Cost Sharing

This refers to the covered person’s share of costs for covered services; these are sometimes called “out-of-pocket costs” or “OOP” costs. Some examples of cost sharing or out-of-pocket costs are deductibles, copayments (also called copays), and coinsurance.

Out-of-Pocket Maximum

An out-of-pocket maximum is the most you have to pay for covered services in a year. Included in this maximum are deductibles, copays, and coinsurance. However, premiums are not included.

After you reach this amount, the insurance company pays 100% of covered services.

Network

A health insurance network includes facilities, providers, and suppliers that a health plan has contracted with to provide health care services. “In-network” providers and facilities are generally cheaper than those that are not in-network (i.e., out-of-network).

Claim

An insurance claim is a request for a benefit (including reimbursement of a health care expense) made by you or your health care provider to your health insurer or plan for items or services you think are covered.

For example, if you have an office visit with a specialist, a claim will be made in order for your insurance plan to reimburse or cover the service. Insurers can approve claims, covering that service or medication, or they can deny claims, essentially denying to cover that service or medication.

Prior Authorization

Some services, treatments, or prescriptions require prior approval (a “prior authorization”) from the health insurer in order to have that service, treatment, or prescription covered by your plan. While not guaranteed, this makes it more likely that your health plan will cover the cost. Services may include hospital admission, planned surgery, imaging tests, or medical equipment.

Navigator

An individual who is trained to assist consumers, businesses, and their employees with evaluating and choosing health insurance plans, as well as completing forms. Navigators may also be referred to as assisters or “promotoras,” for those who work specifically with Spanish-speaking communities.

Now that we have laid a foundation for what some of these health insurance terms mean, let’s look at an example of how to apply this understanding when comparing two different health insurance plans.

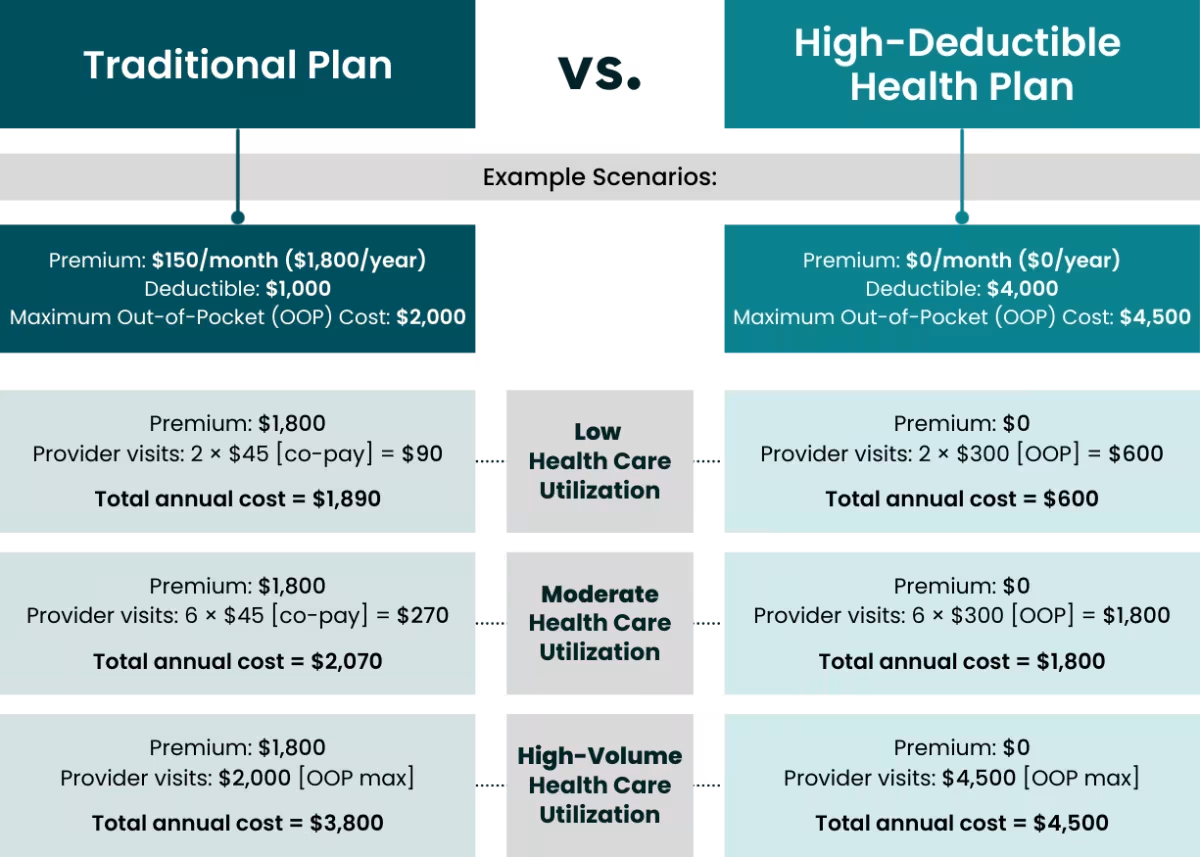

What Is a High-Deductible Health Plan? Traditional Plans vs. High-Deductible Health Plans (HDHPs)

When choosing a health insurance plan, there are multiple things to consider, as certain plans may fit your needs better than others. For example, higher premium costs tend to be paired with lower deductibles. This could be ideal for those who know they will likely use their coverage often, allowing them to reach their deductible quickly. However, those who don’t think they’ll use their coverage often might not want to pay high premiums every month just to have coverage. This is where high-deductible-health plans come in.

A traditional health plan usually has monthly premiums, a deductible, and an out-of-pocket maximum for health expenses.

A high-deductible health plan (HDHP), on the other hand, typically has a low premium (or none at all) but, as the name suggests, a higher deductible, and higher out-of-pocket maximum compared to a traditional health plan. With these plans, enrollees don’t pay a monthly premium (or, if they do, it is generally low) for insurance, but every expense will be paid out-of-pocket until that high deductible is met.

To better understand and compare these two plan types, let’s look at an example of a high-level annual breakdown of costs for each plan for three unique example scenarios: (1) low health care utilization, (2) moderate health care utilization, and (3) high-volume health care utilization.

Note: The amounts below are a composite of common costs from various health plans or average costs for provider visits. This is meant to serve solely as an example—costs will vary depending on your specific plan.

Figure 1. Example Annual Costs of a Traditional Plan vs. a High-Deductible Health Plan

An accessible table alternative to this graphic can be found at the end of this blog.

When considering the choice of a health insurance plan, it is important to assess your predicted health care costs throughout the year. While these examples and numbers are hypothetical, they can offer some insight into the differences between plans for different individuals and situations.

Along with understanding health insurance terminology, evaluating your specific situation, finances, and health care needs is an important part of choosing an insurance plan. Navigators and assisters exist to help guide you through the insurance process - find resources for your state here.

You can also explore data on high-deductible health plans on State Health Compare.

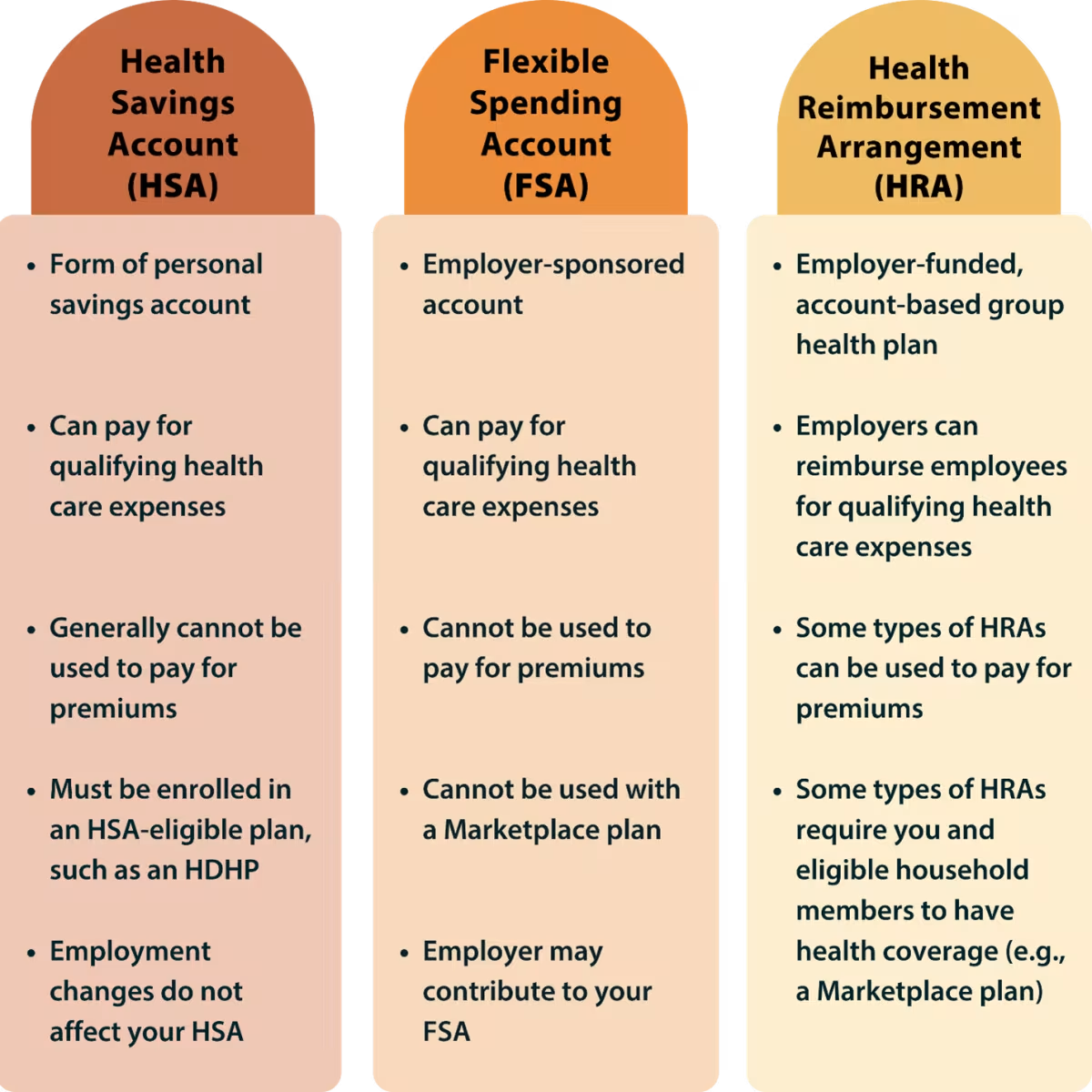

Defining Additional Health Insurance Benefits and Features

In addition to covered services and prescriptions, health insurance plans may also offer additional benefits for their members. Below are definitions of common benefits offered by employers and what they mean in the context of ESI.

Health Savings Account (HSA)

A health savings account (HSA) is a type of pre-tax personal savings account you can set up to pay certain health care costs, such as doctor visits, prescription drugs, and long-term care services. HSAs are usually only offered when enrolled in a HDHP.

Flexible Spending Account (FSA)

A flexible spending account (FSA) is an account you put money into that you use to pay for certain out-of-pocket health care costs, like deductibles, copayments, and coinsurance. Contributions are added before taxes are taken out, reducing your overall taxable income.

Health Reimbursement Arrangement (HRA)

Health reimbursement arrangements (HRAs) are account-based health plans that allow employers to reimburse employees for certain medical expenses. Employees get reimbursed tax-free up to the maximum amount the employer will repay for health care costs within a certain amount of time.

Figure 2. Key Aspects of Health Savings Accounts, Flexible Spending Accounts, and Health Reimbursement Arrangements

While these benefits and features may not be the highest priorities when selecting a health plan, they are important elements and can assist when choosing which one meets your needs.

Health Insurance Terminology and Understanding Health Insurance

Understanding health insurance plans and other employer-offered health benefits may feel overwhelming due to complexities in differentiating elements, costs, benefits, and, of course, health insurance terms.

We hope that the health insurance definitions and explanations we provided in this review help provide clarity for those seeking more information on health insurance and can be a resource for improving health insurance literacy.

For more complex issues in choosing or navigating health insurance plans, your company’s HR or benefits coordinator (if dealing with ESI) can help. If you are looking at an ACA marketplace or Medicaid plan, you can connect with a state navigator or assister.

Check out our catalog of Basics Blogs here to learn more about health policy, public health, and more.

Table 1. Traditional Plan vs. HDHP Example

Example Scenarios | Traditional Plan Premium: $150 per month Deductible: $1,000 Maximum Out-of-Pocket Cost: $2,000

| High-Deductible Health Plan Premium: $0 per month Deductible: $4,000 Maximum Out-of-Pocket Cost: $4,500

|

|---|---|---|

Low Health Care Utilization | Premium: $150 × 12 months = $1,800 Provider visits: 2 × $45 [co-pay] = $90 Total annual cost = $1,890

| Premium: $0 × 12 months = $0 Provider visits: 2 × $300 [out-of-pocket] = $600 Total annual cost = $600

|

Moderate Health Care Utilization | Premium: $150 × 12 months = $1,800 Provider visits: 6 × $45 [co-pay] = $270 Total annual cost = $2,070

| Premium: $0 × 12 months = $0 Provider visits: 6 × $300 [out-of-pocket] = $1,800 Total annual cost = $1,800

|

High-Volume Health Care Utilization | Premium: $150 × 12 months = $1,800 Provider visits: $2,000 [out-of-pocket max] Total annual cost = $3,800

| Premium: $0 × 12 months = $0 Provider visits: $4,500 [out-of-pocket max] Total annual cost = $4,500

|